Coming Up Short

Short sales are here for the long haul

When Realtor Jonathan Osman worked his first short sale in 2007, it was because no one else in his office knew how to do one and a senior agent thought a young, bright upstart like him could figure it out. Two years later, Osman did about a dozen short sales, where the bank agrees to take less from a buyer than what the seller owes on the mortgage to avoid an outright foreclosure.

Last year, that number tripled to about thirty-six for Osman. This year, he says he’s on track to do seventy-five. “Last fall, it just exploded and it hasn’t stopped,” says Osman, of Keller Williams Realty’s SouthPark office.

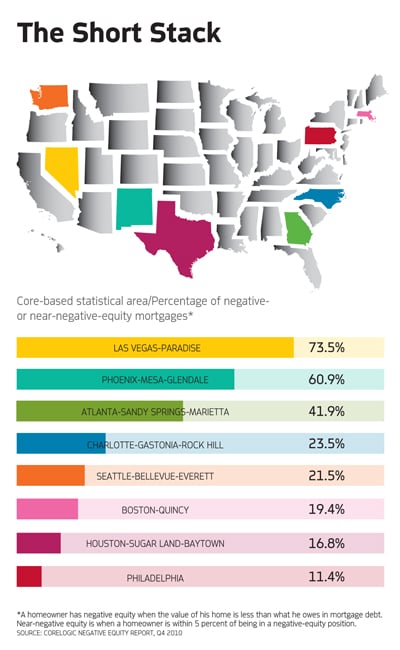

There are no statistics on the number of short sales in the Charlotte area, but real estate agents and lawyers who specialize in the tricky transactions say they’ve seen a recent surge. That’s due to a number of factors that have converged to form a perfect short-sale storm.

After several years of a depressed housing market, banks seem to have the staff and processes in place to handle short sales.

Legal challenges have put a halt to many foreclosures, and the government is encouraging banks to accept short-sale offers from buyers. And, after several years of a depressed housing market, banks seem to finally have the staff and processes in place to handle short sales, says Osman.

Real estate attorney Jaime Kosofsky says banks often prefer short sales to foreclosures, because short sales generally cost them less. But they’re not willing to accept rock-bottom offers for short-sale properties, he says. One rule of thumb: a buyer has to be willing to pay at least 80 percent of an owner’s mortgage debt for the bank to approve a short sale.

Osman says he expects the short sale momentum to continue for several more years. “The market was just very overvalued, and there are lots of people out there who owe more on their mortgage than what it’s worth,” he says. “And it’s going to take a while to get that sorted out.”